“I have a good-paying job and went to a state university on a scholarship. And I’m still paying almost $650 a month for the next 10 years [to repay my student loans]. How is that the price of getting an education and serving others in the healthcare field? If I’m stressed out and have trouble paying more than the minimum on my loans, what about teachers? Or [other] students who start out closer to $30,000 a year?”

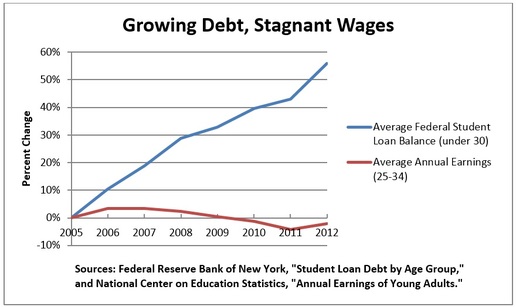

That’s my college friend, Sarah. Though we now live in different parts of the country, we still keep tabs on each other’s fledgling careers. Unfortunately, that means our conversations often include concerns about our burdensome loan debts. And we’re not the only ones — the U.S. Department of Education expects about a fifth of new borrowers to default on their federal student loans at some point during repayment. This is alarming, especially when considering that federal loans account for more than 90 percent of student lending and are held by roughly 40 million Americans.

That’s my college friend, Sarah. Though we now live in different parts of the country, we still keep tabs on each other’s fledgling careers. Unfortunately, that means our conversations often include concerns about our burdensome loan debts. And we’re not the only ones — the U.S. Department of Education expects about a fifth of new borrowers to default on their federal student loans at some point during repayment. This is alarming, especially when considering that federal loans account for more than 90 percent of student lending and are held by roughly 40 million Americans.

One commonly proposed method to curtail high default rates is an income-based repayment (IBR) plan, under which students repay their loans based on a set percentage of their income, rather than paying an arbitrary monthly minimum. Currently, the federal government allows students to make payments capped at 10 percent of their discretionary income. (It also exempts a minimum of $17,505 of the borrower’s income, meaning that 10 percent figure is calculated only from income earned above that threshold.) Payments are made for 10 or 20 years, after which the remaining balance is forgiven. Sounds good, right? Then why do only 14 percent of borrowers opt to use IBR?

According to a new report from New America, Young Invincibles, and the National Association of Student Financial Aid Administrators, the answer is largely because of the administrative burden that IBR places on borrowers. To use current IBR models, borrowers must fill out paperwork to opt in, submit income information from a prior year’s tax return or other sources of income documentation, and reapply annually. Other options eliminate much of that burden by simply calculating monthly payments based on loan amounts and interest rates. While IBR aims to help borrowers avoid default by making their payments more manageable, the additional steps and paperwork currently required under IBR can actually have the reverse effect, increasing the odds of default.

Additionally, because current IBR methods are based on tax returns, the income information used to determine monthly payments can be up to two years old. Many recent graduates also have not filed a tax return by the time their loan repayment begins, or have filed as dependents of their parents. Because of this, payments are often too high or too low, relative to the borrower’s actual current income, the report authors say.

To address these problems, the report suggests a unique IBR system in which borrowers are automatically enrolled, meaning that borrowers would neither have to opt in to the program nor reapply annually. Additionally, this system would be based on payroll withholdings. Rather than asking borrowers to manually make a monthly payment, their employers would automatically withhold the owed amount from their paychecks. This means that borrowers would not have to submit dated information from tax returns; instead, payment amounts would be based directly on their current income. For example, if a borrower earns $48,000 per year (or $4,000 per month) and must repay 10 percent of his or her income for student loans, the employer would automatically withhold $400 from his or her monthly paycheck.

This system would also have its own implementation challenges. It would have to be carefully designed to limit the added burden on employers. It also would require some type of reconciliation process (similar to that used in the federal tax collection system) to address any mismatch between when income is earned versus when it is reported and taxed, as well as account for different ways borrowers earn income. However, if implemented correctly, it would keep payments at an affordable level and remove the heavy administrative burden on borrowers, thereby decreasing the likelihood of default. That would mean recent graduates, like my friend Sarah, can focus on jump-starting their promising careers, rather than stressing over the loans that made them possible.

Phillip Burgoyne-Allen is a legislative assistant at an education law firm. Reach him via email or Twitter.

According to a new report from New America, Young Invincibles, and the National Association of Student Financial Aid Administrators, the answer is largely because of the administrative burden that IBR places on borrowers. To use current IBR models, borrowers must fill out paperwork to opt in, submit income information from a prior year’s tax return or other sources of income documentation, and reapply annually. Other options eliminate much of that burden by simply calculating monthly payments based on loan amounts and interest rates. While IBR aims to help borrowers avoid default by making their payments more manageable, the additional steps and paperwork currently required under IBR can actually have the reverse effect, increasing the odds of default.

Additionally, because current IBR methods are based on tax returns, the income information used to determine monthly payments can be up to two years old. Many recent graduates also have not filed a tax return by the time their loan repayment begins, or have filed as dependents of their parents. Because of this, payments are often too high or too low, relative to the borrower’s actual current income, the report authors say.

To address these problems, the report suggests a unique IBR system in which borrowers are automatically enrolled, meaning that borrowers would neither have to opt in to the program nor reapply annually. Additionally, this system would be based on payroll withholdings. Rather than asking borrowers to manually make a monthly payment, their employers would automatically withhold the owed amount from their paychecks. This means that borrowers would not have to submit dated information from tax returns; instead, payment amounts would be based directly on their current income. For example, if a borrower earns $48,000 per year (or $4,000 per month) and must repay 10 percent of his or her income for student loans, the employer would automatically withhold $400 from his or her monthly paycheck.

This system would also have its own implementation challenges. It would have to be carefully designed to limit the added burden on employers. It also would require some type of reconciliation process (similar to that used in the federal tax collection system) to address any mismatch between when income is earned versus when it is reported and taxed, as well as account for different ways borrowers earn income. However, if implemented correctly, it would keep payments at an affordable level and remove the heavy administrative burden on borrowers, thereby decreasing the likelihood of default. That would mean recent graduates, like my friend Sarah, can focus on jump-starting their promising careers, rather than stressing over the loans that made them possible.

Phillip Burgoyne-Allen is a legislative assistant at an education law firm. Reach him via email or Twitter.

RSS Feed

RSS Feed